Thursday, March 31, 2011

Matt Taibbi is close to loosing faith in Obama

As for Obama, I just disagree that he did all he could, in health care or elsewhere. I just don't fall for the storyline that deep down inside he wants to do all these wonderful progressive things, but is halted by political circumstance. The evidence doesn't support the idea that he actually wants these things, deep down. The evidence does, however, support the idea that he has very effectively marketed himself to progressives as someone who secretly sympathizes with progressives. I have conflicting feelings about Obama, and think there is some good in him still, but I've given up the idea that he could be a champion for any kind of real reform of anything. [source]

Rosenberg Strategies for a Volatile Range-Bound Market

In sum, the six strategies I think are going to make the most sense this year in terms of generating solid risk-adjusted returns are going to be first, an emphasis on large cap and mid cap equities that have, once again, strong balance sheets, payout a consistent dividend stream, stable earnings growth, have relatively low correlations with the U.S. economy. We remain in the camp that believes higher- quality equities will provide more sustainable returns over the intermediate run.

Secondly, commodities, especially the energy sector as well as precious metals, as a hedge against recurring weakness in global currencies makes imminent sense. We’re also constructive on agriculture.

Thirdly, again fixed income securities, especially corporate bonds. We continue to see tremendous opportunities in the high-yield sector in particular.

Fourth, classic diversified hybrids that have low volatility, yields that exceed what anyone can get in the government sector.

Fifth, capital preservation strategies remain a cornerstone.

Lastly, once again emphasis on Canadian dollar investments, as well as a diversification towards the faster-growing emerging markets.

---today

Secondly, commodities, especially the energy sector as well as precious metals, as a hedge against recurring weakness in global currencies makes imminent sense. We’re also constructive on agriculture.

Thirdly, again fixed income securities, especially corporate bonds. We continue to see tremendous opportunities in the high-yield sector in particular.

Fourth, classic diversified hybrids that have low volatility, yields that exceed what anyone can get in the government sector.

Fifth, capital preservation strategies remain a cornerstone.

Lastly, once again emphasis on Canadian dollar investments, as well as a diversification towards the faster-growing emerging markets.

---today

Extend and Pretend - the details

Jim Quinn/Minyanville:

...billions in commercial loans are in distress right now because tenants are dropping like flies. Rather than writing down the loans, banks are extending the terms of the debt with more interest reserves included so they can continue to classify the loans as “performing.” The reality is that the values of the property behind these loans have fallen 43%. Banks are extending loans that they would never make now, because borrowers are already grossly upside-down.... About two-thirds of commercial real-estate loans maturing at banks from now through 2015 are underwater... there are 900 banks essentially insolvent, sitting on the FDIC “Problem” list. This is after closing the 300 banks. There are at least a couple hundred billion of losses in the pipeline

One year ago the website www.businessinsider.com listed the 10 major regional banks with the highest risk from commercial real estate loans. These 10 banks had $133 billion of commercial real estate loans on their books...those real estate loans are worth 30% to 50% less than they are being carried on the books. A true valuation of these loans would put all 10 of these banks out of business.

These four "too big to fail" banks have $340 billion of commercial real estate loans on their books. That’s a lot of extending and pretending. Just properly valuing those loans at their true market value would wipe out most of their loan loss reserves....These four banks have $1.1 billion of outstanding mortgage debt on their books. I wonder what a 20% further decline in home prices will do to these loans. Throw in another half a billion of credit card loans...

...billions in commercial loans are in distress right now because tenants are dropping like flies. Rather than writing down the loans, banks are extending the terms of the debt with more interest reserves included so they can continue to classify the loans as “performing.” The reality is that the values of the property behind these loans have fallen 43%. Banks are extending loans that they would never make now, because borrowers are already grossly upside-down.... About two-thirds of commercial real-estate loans maturing at banks from now through 2015 are underwater... there are 900 banks essentially insolvent, sitting on the FDIC “Problem” list. This is after closing the 300 banks. There are at least a couple hundred billion of losses in the pipeline

One year ago the website www.businessinsider.com listed the 10 major regional banks with the highest risk from commercial real estate loans. These 10 banks had $133 billion of commercial real estate loans on their books...those real estate loans are worth 30% to 50% less than they are being carried on the books. A true valuation of these loans would put all 10 of these banks out of business.

These four "too big to fail" banks have $340 billion of commercial real estate loans on their books. That’s a lot of extending and pretending. Just properly valuing those loans at their true market value would wipe out most of their loan loss reserves....These four banks have $1.1 billion of outstanding mortgage debt on their books. I wonder what a 20% further decline in home prices will do to these loans. Throw in another half a billion of credit card loans...

The Brave New World

In the UK (Jesse Eisinger):

...major government figures speak openly about requiring substantially higher bank capital. The governor of the Bank of England, the head of the Financial Services Authority (the equivalent of the Securities and Exchange Commission) and even the conservative chancellor of the Exchequer have backed a bigger crackdown on the banking sector. While the international banking rules, called Basel III, settled on 7 percent as the minimum standard for a certain kind of capital, it’s acceptable in Britain to talk about having significantly higher standards. A recent Bank of England paper contemplated capital on the order of 15 to 20 percent.=

In the US (Barry Ritholtz):

...major government figures speak openly about requiring substantially higher bank capital. The governor of the Bank of England, the head of the Financial Services Authority (the equivalent of the Securities and Exchange Commission) and even the conservative chancellor of the Exchequer have backed a bigger crackdown on the banking sector. While the international banking rules, called Basel III, settled on 7 percent as the minimum standard for a certain kind of capital, it’s acceptable in Britain to talk about having significantly higher standards. A recent Bank of England paper contemplated capital on the order of 15 to 20 percent.=

In the US (Barry Ritholtz):

- The banks own Congress

- Regulators have long been captured

- 7% capital reserves = 14 to 1 leverage is unacceptable to banks (pre-crisis levels used to be 12 to 1 before waivers were granted)

- The Obama White House, tainted by Robert Rubin pro-bank staffing recommendations, missed their window to really fix what is broken on Wall Street.

- Another major financial crisis is inevitable

Wednesday, March 30, 2011

What does Joe Klein at Time think about Republicans?

"This is my 10th presidential campaign, Lord help me. I have never before seen such a bunch of vile, desperate-to-please, shameless, embarrassing losers coagulated under a single party's banner. They are the most compelling argument I've seen against American exceptionalism. Even Tim Pawlenty, a decent governor, can't let a day go by without some bilious nonsense escaping his lizard brain. And, as Greg Sargent makes clear, Mitt Romney has wandered a long way from courage. There are those who say, cynically, if this is the dim-witted freak show the Republicans want to present in 2012, so be it. I disagree. One of them could get elected. You never know. Mick Huckabee, the front-runner if you can believe it, might have to negotiate a trade agreement, or a defense treaty, with the Indonesian President some day. Newt might have to discuss very delicate matters of national security with the President of Pakistan. And so I plead, as an unflinching American patriot--please Mitch Daniels, please Jeb Bush, please run. I may not agree with you on most things, but I respect you. And you seem to respect yourselves enough not to behave like public clowns."

---Source, via DeLong

---Source, via DeLong

Consumer confidence down

Following in the footsteps of the University of Michigan survey, the Conference Board survey showed an 8.6 point slide in consumer confidence in March to a three month low of 63.4. Out of the nine regions, seven were down, one was up and one was flat. Interestingly, even with all the bad global news, the “present situation” component managed to rise from 33.8 to 36.9 in March, the best print since November 2008. But what drives consumer spending is the “expectations” component, and it sank to 81.1 from 97.5, a four-month low. The “jobs are plentiful” index fell to 4.4 from 4.9, while “jobs hard to get” rose to 44.6 from 44.4. So all in, the net jobs index deteriorated 0.7 of a point and suggests that we should at least see a rebound in the unemployment rate in Friday’s jobs report. Buying plans were down right across the board: Home buying plans have gone from 5.2% in January, to 4.9% in February, to 3.8% in March. Auto intentions sagged to 10.9% from 12.8% in February. Plans to buy a major appliance took a real licking — down to 42% from 47.5%, while vacation plans sagged to 45.5% from 51.1%. This is a tale of woes as it pertains to the outlook for discretionary consumer spending...

There is the old saying of how one should focus on what consumers do as opposed to what they say they will do. But we are seeing real consumer spending running at a 1% annual rate so far in Q1, which is well below the 4% pace in the fourth quarter. And the chain store sales data are coming in below plan ― so far +2.2% YoY versus +2.5% planned. Discount stores are surprising on the upside, department stores on the downside.

---ibid

There is the old saying of how one should focus on what consumers do as opposed to what they say they will do. But we are seeing real consumer spending running at a 1% annual rate so far in Q1, which is well below the 4% pace in the fourth quarter. And the chain store sales data are coming in below plan ― so far +2.2% YoY versus +2.5% planned. Discount stores are surprising on the upside, department stores on the downside.

---ibid

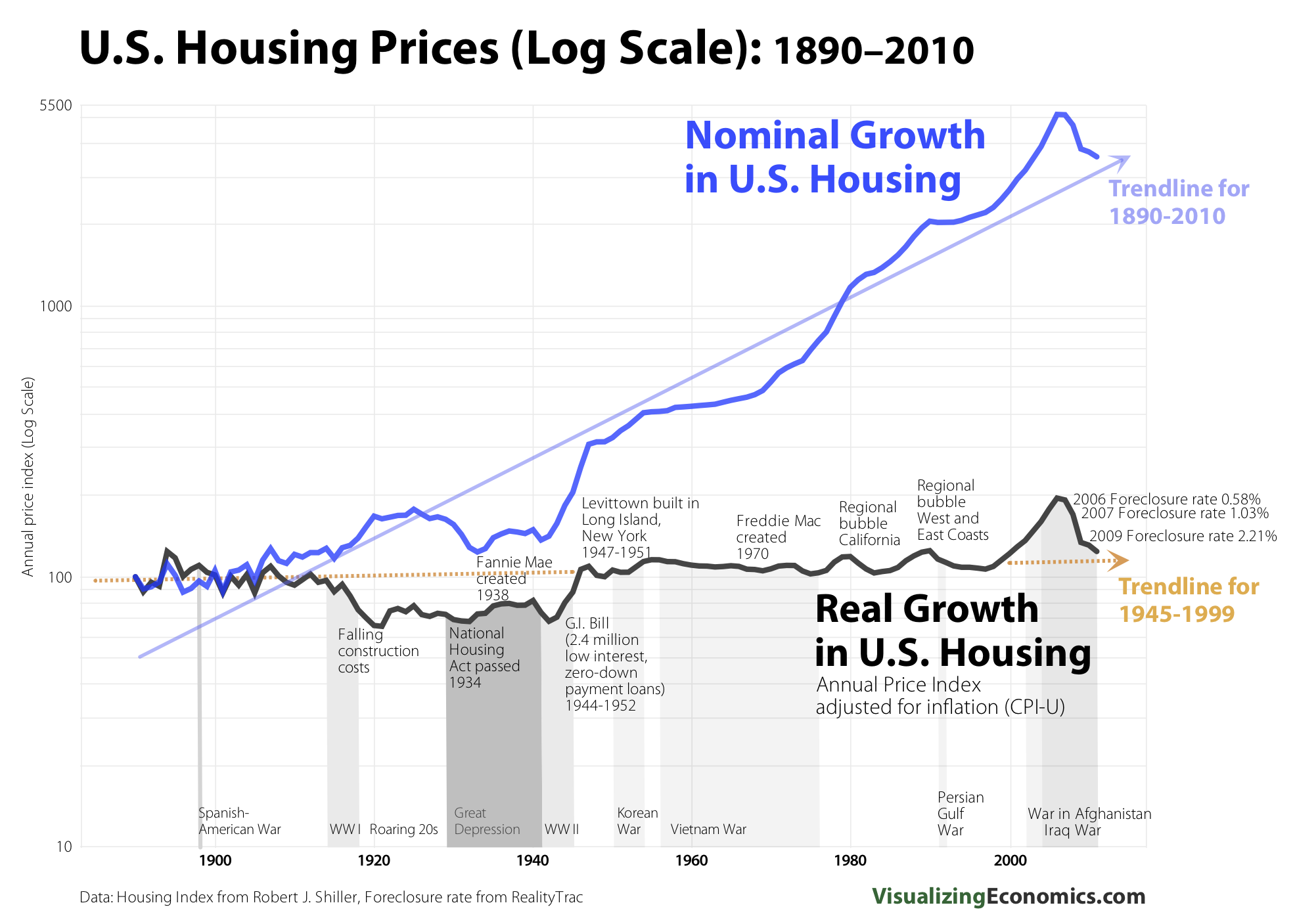

Rosenberg Daily - The week in housing

today:

The best that can be said about the Case-Shiller index is that it didn’t come in as bad as the consensus had thought, but even so, the 20-city measure was down 1% yet again (and down in 19 of the 20 cities) on a non-seasonally adjusted basis and off 0.2% seasonally adjusted — the seventh decline in a row. Over that time frame prices have fallen at an 8% annual rate, which in wealth effect terms on spending is equivalent to a 15% correction in the equity market. As the chart below shows, we are just 1% away from the price level itself breaking below the April 2009 lows — in fact, the last time we had prices decline this much (8%) over a seven-month span was back in June 2009, at the depths of the worst recession since the 1930s.

Demand for home ownership is undergoing a profound structural change. As one would expect considering that one in seven Americans with a mortgage are still either in the arrears process or in outright foreclosure. This, heading into the third year of a statistical economic expansion, is incredible. The fact that Lennar reported a 12% slide in year-over-year orders despite vastly improved affordability levels just about says it all. We could well see even lower lows in single family starts in coming months.

...The sluggish first-time buyer is one of the reasons the housing market can’t move off the ground floor (basement?). Only 34% of existing home sales were accounted for by first-time home-buyers last month whereas a normal market typically sees that ratio closer to 45%. Don’t be fooled by survey data ―mortgage credit standards are tightening and that can be seen vividly in the fact that loans in Freddie Mac’s portfolios now have an average FICO score of 758 from 720 a year ago (as per the USA Today). The best mortgage terms are saved for those with at least a 20% downpayment (there is a whole class of borrowers who have to Google that term since it was stricken from the mortgage market lexicon during the bubble). At the same time, regulators are reportedly going to be mandating that banks maintain a 5% threshold for risk on mortgage securities. Add to that the aggressive move by the House Republicans to wind down Fanny and Freddie much more quickly than the White House had been proposing (see In Congress, Bills to Speed Unwinding of 2 Giants in today’s NYT). And we just heard from Chicago Federal Reserve Board President Evans that one of the ways the Fed will be shrinking its balance sheet (QE3 does not look like it’s in the cards) would be by selling down its $940 billion cache of mortgage-backed securities.

The best that can be said about the Case-Shiller index is that it didn’t come in as bad as the consensus had thought, but even so, the 20-city measure was down 1% yet again (and down in 19 of the 20 cities) on a non-seasonally adjusted basis and off 0.2% seasonally adjusted — the seventh decline in a row. Over that time frame prices have fallen at an 8% annual rate, which in wealth effect terms on spending is equivalent to a 15% correction in the equity market. As the chart below shows, we are just 1% away from the price level itself breaking below the April 2009 lows — in fact, the last time we had prices decline this much (8%) over a seven-month span was back in June 2009, at the depths of the worst recession since the 1930s.

Demand for home ownership is undergoing a profound structural change. As one would expect considering that one in seven Americans with a mortgage are still either in the arrears process or in outright foreclosure. This, heading into the third year of a statistical economic expansion, is incredible. The fact that Lennar reported a 12% slide in year-over-year orders despite vastly improved affordability levels just about says it all. We could well see even lower lows in single family starts in coming months.

...The sluggish first-time buyer is one of the reasons the housing market can’t move off the ground floor (basement?). Only 34% of existing home sales were accounted for by first-time home-buyers last month whereas a normal market typically sees that ratio closer to 45%. Don’t be fooled by survey data ―mortgage credit standards are tightening and that can be seen vividly in the fact that loans in Freddie Mac’s portfolios now have an average FICO score of 758 from 720 a year ago (as per the USA Today). The best mortgage terms are saved for those with at least a 20% downpayment (there is a whole class of borrowers who have to Google that term since it was stricken from the mortgage market lexicon during the bubble). At the same time, regulators are reportedly going to be mandating that banks maintain a 5% threshold for risk on mortgage securities. Add to that the aggressive move by the House Republicans to wind down Fanny and Freddie much more quickly than the White House had been proposing (see In Congress, Bills to Speed Unwinding of 2 Giants in today’s NYT). And we just heard from Chicago Federal Reserve Board President Evans that one of the ways the Fed will be shrinking its balance sheet (QE3 does not look like it’s in the cards) would be by selling down its $940 billion cache of mortgage-backed securities.

Bush was right! The way to salvation is through flat-screen TV's!

Krugman today: ...the only way the economy can avoid taking a hit from government cuts is if private spending rises to fill the gap — and although you rarely hear the austerians admitting this, the only way that can happen is if people take on more debt.

There is no private mortgage market

“Under the new regulations, so long as Freddie Mac and Fannie Mae stay in conservatorship, banks will be able to continue to sell them mortgages without having skin in the game.”

That quote, taken from financial media reports on yesterday's new rules for “qualified residential mortgages” (QRM’s) says it all, particularly with 90% of all mortgages today being purchased by the Agencies. ---Proprietary source.

---

I've been saying this in different ways for quite a while. (recently)

That quote, taken from financial media reports on yesterday's new rules for “qualified residential mortgages” (QRM’s) says it all, particularly with 90% of all mortgages today being purchased by the Agencies. ---Proprietary source.

---

I've been saying this in different ways for quite a while. (recently)

Barry Ritholtz begins to understand CNBC

Ritholtz today: I am aghast.

I am watching Squawk Box, and the stream of misstatements, political jargon, and sheer falsity is overwhelming me.

Let me clarify this for you, Joe Kernan: You want to know what the biggest threat to the economy in a century was? RECKLESS OVERLEVERAGED, UNDER-CAPITALIZED BANKERS and the COLLAPSE OF THE FINANCIAL SYSTEM THEY CAUSED.

Remember that little glitch? I know it was a long time ago wat back in 2009, but THAT is and remains the biggest threat to the economy.

I am watching Squawk Box, and the stream of misstatements, political jargon, and sheer falsity is overwhelming me.

Let me clarify this for you, Joe Kernan: You want to know what the biggest threat to the economy in a century was? RECKLESS OVERLEVERAGED, UNDER-CAPITALIZED BANKERS and the COLLAPSE OF THE FINANCIAL SYSTEM THEY CAUSED.

Remember that little glitch? I know it was a long time ago wat back in 2009, but THAT is and remains the biggest threat to the economy.

Tuesday, March 29, 2011

Stiglitz seems to not like Bowles-Simpson

The Bowles-Simpson recommendations, if adopted, would constitute a near-suicide pact: Growth would slow, tax revenues would diminish, the improvement in the deficit would be minimal. ---via DeLong. Excellent points made there.

EPA is considering drastically raising the amount of allowable radiation in food, water and the environment.

Yves Smith: ...some government scientists and media shills are now “reexamining” old studies that show that radioactive substances like plutonium cause cancer to argue that prevent cancer.

It is not just bubbleheads like Ann Coulter saying this. Government scientists from the Pacific Northwest National Laboratories and pro-nuclear hacks like Lawrence Solomon are saying this.

In other words, this is a concerted propaganda campaign to cover up the severity of a major nuclear accident by raising acceptable levels of radiation and saying that a little radiation is good for us.

Yet another market warning

The bounce in the S&P 500 has taken place on very low volume. While markets can move higher on light volume, it is to us indicative of confusion and a lack of confidence on both the bulls and bear to engage the market. ---Barry Ritholtz today

Sunday, March 27, 2011

Housing: Not getting better soon

Ritholtz: As low as rates are, they cannot make up for the lack of wage gains, the massive deleveraging, and the ongoing foreclosure activities.

Friday, March 25, 2011

Rosenberg Daily - Economy Loosing Momentum

As was the case in 2010, the odds are very high that this quarter’s growth rate will prove to be the high-water mark of the year.

The difference is that GDP expanded at a 3.7% annual rate in the first quarter of 2010; however, this time, we are looking at something that is likely closer to 2.5%. The market’s ability to shrug adverse economic news is going to be receiving a very critical test in coming months.

The difference is that GDP expanded at a 3.7% annual rate in the first quarter of 2010; however, this time, we are looking at something that is likely closer to 2.5%. The market’s ability to shrug adverse economic news is going to be receiving a very critical test in coming months.

- Housing activity in the U.S. is taking a new and rather significant leg down; sales, prices and starts.

- Real average weekly earnings have contracted in each of the past four months as wage growth lags the surge in food and fuel prices. According to various surveys, three-quarters of U.S. consumers say they are about to radically cut the discretionary segment of the family budget. Perhaps the 4.6% drop in Best Buy’s same-store sales that was just reported is an early signpost of what’s happening to the “nonessential” part of the family budget.

- The Architectural Billings Index is flagging a renewed decline in commercial construction. State and local government spending on goods and services are being sliced at an unprecedented rate. For a sign of how social contracts (a.k.a. union concessions) are being rewritten even in the most “liberal” of jurisdictions, have a look at Los Angeles, Unions Reach Deal on page A2 of today’s WSJ.

- Federal government stimulus is about to morph into restraint beginning next quarter.

- Sadly, last year’s lynchpin, capital spending, is turning back down. At some point, the ISM manufacturing index will reflect this downturn (it is a survey, while orders and shipments are actual dollars and cents).

---today

Thursday, March 24, 2011

Wednesday, March 23, 2011

Rosenberg Daily - Wait to buy stocks

The Tobin Q, which can be derived from the Fed Flow of Funds report, shows that the market value of equities is over 10% higher than the replacement cost, and the Shiller cyclically-adjusted P/E ratio is some 40% above its long-run norm. Besides, history shows that the market often sputters in year three of a dramatic 100% rebound in the S&P 500 ... so best to wait for better buying opportunities, which are sure to come. ---today

Boockvar: Bad housing news good

Feb New Home sales, a measure of contract signings of new homes, totaled 250k, the lowest on record dating back to 1963 and 40k below expectations. Sales in all 4 regions fell. To put into perspective, US population size in 1963 was 190mm vs 310mm today. In Jan 1963, new home sales totaled 591k. With the sales drop and stable level of homes for sale (186k), the months supply rose to 8.9 from 7.4, the most since Aug. The median price fell 8.9% y/o/y and 13.9% sequentially. Builders continue to face large competition from still too many existing homes on the market, and while they continue to suffer thru a very difficult time, I repeat my comment from last week when Housing Starts were poor that the bright side of this low level of new home sales is that hopefully it allows the market to further purge itself of the inventory of existing homes as we don’t need more new homes right now.

---Peter Boockvar

---Peter Boockvar

Market: February 18 highs are likely the highs for the year

All you hear on financial television are the cheerleaders who tout that the bull market is alive and well. I have disagreed with this notion saying that the February 18 highs are the highs for the year. The Dow declined 6.7% from its February 18 high at 12,391.29 to its March 16 low of 11,555.48, and the rebound over the past four sessions has been 4.0% leaving the Industrials 3.0% below the February high. The NASDAQ declined 8.3% from its February high at 2840.51 to its March 16 low of 2603.50, and the rebound over the past four sessions has been 3.1% leaving the NASDAQ 5.5% below its February high. The NASDAQ ended last week with a negative weekly chart, which stays negative on a close this week below 2725. [More detail at link]

---Richard Suttmeier, chief market strategist at ValuEngine.com

---Richard Suttmeier, chief market strategist at ValuEngine.com

Market will drop without more QE come June

The last Vitus Update had a comment about QE and the recent market rise:

Basically the market is in wait-mode until June, to see if there will be any more QE's coming from the Fed; the current batch runs out then. A lot of the down-sliding of late in the DOW and S&P is directly attributable to the fact that people are starting to bet that not much more QE will be forthcoming. If you don't see more QE, you can fuggedaboud 40% of the 100% rise in the averages since March of '09. Ie, an S&P of about 1050 is quite possible by year-end.Mish today has a good, detailed post making the same point:

All things considered, but especially jobs, housing, and petroleum usage, there is solid evidence we are in the midst of a stimulus-fed financial recovery as opposed to a recovery in any real sense of the word.

When the stimulus dies, the recovery will die with it.

Mish: Gallup Poll Pegs Unemployment Rate at 10.2%, Underemployment at 19.9%, Same as Last Year

[More at link] I [Mish] am very skeptical of BLS unemployment rates inching lower. Not only do the BLS reports discount millions of marginally attached and discouraged workers but BLS seasonal adjustments seem more than a bit unusual.

Gallup polls paint a far different picture. Please consider Gallup Finds U.S. Unemployment at 10.2% in Mid-March

Unemployment Rate

Part-Time Workers Wanting Full-Time Job

Underemployment

Gallup polls paint a far different picture. Please consider Gallup Finds U.S. Unemployment at 10.2% in Mid-March

Unemployment Rate

Part-Time Workers Wanting Full-Time Job

Underemployment

Health Care is not the Shoe Business

One refrain you heard incessantly during the health care reform debate was that we have high health care costs because of overconsumption and we have overconsumption because people don’t bear a high enough share of their marginal health care costs, so the solution is to increase copays and deductibles. This is what Economics 101 would tell you: people respond to incentives. But...one large company that tried this year after year, but only saw their costs going up. The problem was that while most members responded to the higher copays and kept their costs more or less steady, the 5 percent of members who generated 60 percent of the costs behaved differently. Or, rather, they also reduced consumption (of doctor’s visits and prescription medications), but as a result they often had catastrophic outcomes. These were people with heart disease on cholesterol-lowering medications, and when they went off their medications they ended up in the hospital with heart attacks and then with congestive heart failure.

---James Kwak

---James Kwak

The Doom Loop: Banking System Becoming Too Big To Save

Simon Johnson of The Baseline Scenario has a post at Project Syndacate which makes several good points in follow-up to his book 13 Bankers which argues that banks should be down-sized:

...the financial sector in the US and globally has become much more unstable in recent decades, and there is nothing in any of the reform efforts undertaken since the near-meltdown in 2008 that will make it safer.

People sometimes talk about “systemic risk” as if it were intrinsic to the financial system. But modern financial history, including in emerging markets, strongly indicates otherwise...

The three people who have articulated this problem most clearly include two of the world’s leading central bankers. Before Ben Bernanke became Chairman of the Federal Reserve Board, he was rightly renowned for his academic work on the Great Depression, which showed how, under the right (or wrong) conditions, the financial sector could act as a form of accelerant for developments in the real (nonfinancial) economy...

Anat Admati, a professor at Stanford’s Graduate School of Business, focuses on bank capital – specifically, the incentives that banks have to fund their activities with very high leverage – little equity and a great deal of debt. In my view, she has the single most important page on the Web today (http://www.gsb.stanford.edu/news/research/admati.etal.mediamentions.html), containing both original research by her, Peter deMarzo, Martin Hellwig, and Paul Pfleiderer and their many interventions in the policy debate...

Mervyn King, a former academic who is currently Governor of the Bank of England, and his colleagues have a vivid name for the toxic cocktail that results: “doom loop.” The idea is that every time the financial system is in trouble, it receives a great deal of support from central banks and government budgets. This limits losses to stockholders and completely protects almost all creditors...

America’s too-big-to-fail banks are well on their way to becoming too big to save. That point will be reached when saving the big banks, protecting their creditors, and stabilizing the economy plunges the US government so deeply into debt that its solvency is called into question, interest rates rise sharply, and a fiscal crisis erupts.

...the financial sector in the US and globally has become much more unstable in recent decades, and there is nothing in any of the reform efforts undertaken since the near-meltdown in 2008 that will make it safer.

People sometimes talk about “systemic risk” as if it were intrinsic to the financial system. But modern financial history, including in emerging markets, strongly indicates otherwise...

The three people who have articulated this problem most clearly include two of the world’s leading central bankers. Before Ben Bernanke became Chairman of the Federal Reserve Board, he was rightly renowned for his academic work on the Great Depression, which showed how, under the right (or wrong) conditions, the financial sector could act as a form of accelerant for developments in the real (nonfinancial) economy...

Anat Admati, a professor at Stanford’s Graduate School of Business, focuses on bank capital – specifically, the incentives that banks have to fund their activities with very high leverage – little equity and a great deal of debt. In my view, she has the single most important page on the Web today (http://www.gsb.stanford.edu/news/research/admati.etal.mediamentions.html), containing both original research by her, Peter deMarzo, Martin Hellwig, and Paul Pfleiderer and their many interventions in the policy debate...

Mervyn King, a former academic who is currently Governor of the Bank of England, and his colleagues have a vivid name for the toxic cocktail that results: “doom loop.” The idea is that every time the financial system is in trouble, it receives a great deal of support from central banks and government budgets. This limits losses to stockholders and completely protects almost all creditors...

America’s too-big-to-fail banks are well on their way to becoming too big to save. That point will be reached when saving the big banks, protecting their creditors, and stabilizing the economy plunges the US government so deeply into debt that its solvency is called into question, interest rates rise sharply, and a fiscal crisis erupts.

Tuesday, March 22, 2011

Rosenberg investing themes du jour

- Gold and silver

- Energy exposure, especially oil and the drillers

- Canadian dollar denominated corporate bonds

- Hybrids with oil/gas paper content and a running yield that exceeds U.S. Treasuries

- Hedge funds that hedge — relative value trades

- Emerging debt and equity markets, selectively — value has opened up recently

- Japanese equities for value too ... recession is already priced in • Staples over cyclicals; strong balance sheets over weak; large caps over

- small caps

- Various muni bonds — states in areas where the economic base is linked to energy and food such as Texas, Kansas, Iowa, and Missouri — what Meredith Whitney dubs “the emerging markets of the U.S.A.”

Monday, March 21, 2011

The Recent Greenspan Thing: Krugman and DeLong waste time

As Yves Smith would say: Bill here...

Matt Taibbi in his book Griftopia has an excellent section on Greenspan and the roots of his now (in)famous religiositc belief in the almighty power of Markets. "Dr." Greenspan, in a recent paper, is back energetically defending his beloved Free Markets, despite admitting before congress in October, 2008, that in effect, the ideal of totally free markets does not work in practice. In the paper, The Doctor attempts to blame the continuing recession on Obama and government interference with markets, which he calls "activism".

It seems that any faint whiff of an effort of people trying to protect themselves by suggesting regulation of the financial system brings Greenspan to the Barricades in defense of Markets (Suggestion, not hard rules, is the base mechanism of Dodd-Frank). It is left as an exercise for the reader to disentangle the argument of why, if markets are so all-powerful, they need such vigorous defense. (I'm not the first person to point this out)

Prominent economists Paul Krugman and Brad DeLong among others have deconstructed Greenspan's paper. Krugman is brief, and DeLong extensive, and both are recommended, despite the headline above.

I (as usual?) have couple of observations much more earthy than DeLong or Krugman on the stupidness of the Greenspaner's latest:

Matt Taibbi in his book Griftopia has an excellent section on Greenspan and the roots of his now (in)famous religiositc belief in the almighty power of Markets. "Dr." Greenspan, in a recent paper, is back energetically defending his beloved Free Markets, despite admitting before congress in October, 2008, that in effect, the ideal of totally free markets does not work in practice. In the paper, The Doctor attempts to blame the continuing recession on Obama and government interference with markets, which he calls "activism".

It seems that any faint whiff of an effort of people trying to protect themselves by suggesting regulation of the financial system brings Greenspan to the Barricades in defense of Markets (Suggestion, not hard rules, is the base mechanism of Dodd-Frank). It is left as an exercise for the reader to disentangle the argument of why, if markets are so all-powerful, they need such vigorous defense. (I'm not the first person to point this out)

Prominent economists Paul Krugman and Brad DeLong among others have deconstructed Greenspan's paper. Krugman is brief, and DeLong extensive, and both are recommended, despite the headline above.

I (as usual?) have couple of observations much more earthy than DeLong or Krugman on the stupidness of the Greenspaner's latest:

- Here, I said

I've seen a number of articles (here, here), which say that the reason small businesses, the well-known primary generator of jobs, aren't hiring is that there are no customers. I've not heard or seen or imagined any small business owner saying to herself 'Say, if I could just get a tax rate reduction, I'd hire a bunch of people'. ...if you've ever been in a small business, you know that taxes, minimum wages, etc, are secondary or tertiary issues to consider in running the business and hiring.

The argument that rules, taxes, etc, are responsible for any change in economic activity is highly suspect. A suggestion that such things might be responsible for the Great Recession, is just stupid. Not ignorant - stupid. - "Dr." G's paper is 17 pages long. Well, it looks like an academic paper - there are quite a few graphs! No equations, but maybe this paper is for casual readers. It's published by Wiley; the Editorial Advisory board includes some heavyweights including Barry Eichengreen, Menzie Chinn, and Williem Buiter (yikes! R Glenn Hubbard too...). Typical articles have the typical 20 plus or minus references. G's paper has five references, two of them by Dr. Alan Greenspan. Of interest to me, the other three references are from 2004 or so. The financial crisis never happened. I feel much better.

Sunday, March 20, 2011

Why does this resonate with me so much?

Wikipedia: The Dunning–Kruger effect is a cognitive bias in which unskilled people make poor decisions and reach erroneous conclusions, but their incompetence denies them the metacognitive ability to appreciate their mistakes.[1] The unskilled therefore suffer from illusory superiority, rating their ability as above average, much higher than it actually is, while the highly skilled underrate their own abilities, suffering from illusory inferiority...

it is clear from Dunning's and others' work that many Americans, at least sometimes and under some conditions, have a tendency to inflate their worth. It is interesting, therefore, to see the phenomenon's mirror opposite in another culture. In research comparing North American and East Asian self-assessments, Heine of the University of British Columbia finds that East Asians tend to underestimate their abilities, with an aim toward improving the self and getting along with others.

---via Ritholtz, discussing one Alan Greenspan

it is clear from Dunning's and others' work that many Americans, at least sometimes and under some conditions, have a tendency to inflate their worth. It is interesting, therefore, to see the phenomenon's mirror opposite in another culture. In research comparing North American and East Asian self-assessments, Heine of the University of British Columbia finds that East Asians tend to underestimate their abilities, with an aim toward improving the self and getting along with others.

---via Ritholtz, discussing one Alan Greenspan

Another good "is Japan safe" report

Paul Blustein Via Brad DeLong

Particularly because we don’t live in the immediate vicinity of the nuclear plants, we’re confident that we’re as safe here as always — which is to say, extremely safe, the kind of safe that makes us comfortable sending our fourth-grader on a long train and bus commute to school, a fairly common routine here even for much younger children. Aftershocks, power outages, panic food-buying, long gasoline lines — this, too, will pass, and it’s hard to pity ourselves much given the misery that people along Japan’s northeast coast have endured since March 11.

If there is anything to worry about, it is that the perception of Japan as an unsafe country will inflict all kinds of economic and psychological damage. That would compound the tragedy it is enduring, hamper its ability to recover and elevate the challenges it faces just when it is most in need of support..

Particularly because we don’t live in the immediate vicinity of the nuclear plants, we’re confident that we’re as safe here as always — which is to say, extremely safe, the kind of safe that makes us comfortable sending our fourth-grader on a long train and bus commute to school, a fairly common routine here even for much younger children. Aftershocks, power outages, panic food-buying, long gasoline lines — this, too, will pass, and it’s hard to pity ourselves much given the misery that people along Japan’s northeast coast have endured since March 11.

If there is anything to worry about, it is that the perception of Japan as an unsafe country will inflict all kinds of economic and psychological damage. That would compound the tragedy it is enduring, hamper its ability to recover and elevate the challenges it faces just when it is most in need of support..

Saturday, March 19, 2011

Inflation

The problem for the Fed in terms of moving as quickly as June to extend quantitative easing is that we are going through a period of higher measured inflation rates. This is no longer December 2008 or August 2010 when deflation was a legitimate threat. That is clearly not the case now, at least as far as the Producer Price Index (PPI) and Consumer Price Index (CPI) statistics are concerned. We don’t expect to see a real inflation cycle taking hold until we either close the massive resource gap in the jobs market or until the next secular credit expansion takes hold, and that can be years away. But the surge in commodity prices — the Fed actually played a minor role here — is showing through definitively in the price statistics and several measures of inflation expectations are ticking up. Since the central bank has so often in the past talked about these measures it would seem inconsistent to ignore them in a bid to support asset prices once again...

We don’t expect the inflation bulge to last for long, but certainly long enough to push the Fed to the sidelines once QE2 runs its course. Again, not just the actual inflation data, but the 5-year breakeven levels from the TIPS market have risen more than 30 basis points since the end of 2010, and the University of Michigan 5-to- 10-year median inflation expectation index has broken out visibly to the upside, from 2.8% in December, to 2.9% in January and February, to 3.2% in March — the highest since August 2008.

In fact, the Fed tried to generate inflation but it got the wrong kind of inflation. It didn’t get wage inflation, which helps people in their spending plans. It didn’t generate real estate inflation even if it did ignite the stock market for a few months in any event. Instead, what we have are soaring prices for the items that are very difficult to substitute away from like energy and food — that’s the inflation we have.

---ibid [my italics]

We don’t expect the inflation bulge to last for long, but certainly long enough to push the Fed to the sidelines once QE2 runs its course. Again, not just the actual inflation data, but the 5-year breakeven levels from the TIPS market have risen more than 30 basis points since the end of 2010, and the University of Michigan 5-to- 10-year median inflation expectation index has broken out visibly to the upside, from 2.8% in December, to 2.9% in January and February, to 3.2% in March — the highest since August 2008.

In fact, the Fed tried to generate inflation but it got the wrong kind of inflation. It didn’t get wage inflation, which helps people in their spending plans. It didn’t generate real estate inflation even if it did ignite the stock market for a few months in any event. Instead, what we have are soaring prices for the items that are very difficult to substitute away from like energy and food — that’s the inflation we have.

---ibid [my italics]

Rally at an End

It seems clear that from a technical perspective, the uptrend that began in early July has come to an end... The minimum retracement expectation of the July–February rally would be 0.382 or 1,217 on the S&P 500. The more common 0.618 retracement would suggest a move to slightly below 1,140...

If we see some sort of resolution to the crisis in Japan, we should see a nice short-term bounce in the equity market. We are very close to seeing initial support levels kick in for the S&P 500, which would warrant a less negative stance. But any “good news” rally is likely to be brief because as I mentioned in the first paragraph, the trend lines have been broken this time around.

---ibid

If we see some sort of resolution to the crisis in Japan, we should see a nice short-term bounce in the equity market. We are very close to seeing initial support levels kick in for the S&P 500, which would warrant a less negative stance. But any “good news” rally is likely to be brief because as I mentioned in the first paragraph, the trend lines have been broken this time around.

---ibid

Friday, March 18, 2011

Rosenberg Daily (He's Baaaaak) - Real Wages

Once the effects of fiscal stimuli wear off, this negative income trend will show through in a much more visible slowing in real consumer spending that we doubt the markets have fully discounted. So far, what has happened in equities has been treated as a financial event — just wait until the economic event follows suit.

Update 3/19: I [Rosie] pointed out in early March that the most recent nonfarm payroll report, while interpreted as quite bullish by the masses, was really a disappointing post-January rebound that left the January- February average at +128k, little changed from the anaemic pace we had been seen since last fall. Yes, the unemployment rate has been falling thanks to the dwindling ranks of the labour force as those who had been receiving extended jobless benefits fall through the cracks — absent the decline in the participation rate this cycle, the unemployment rate would be sitting at 12% right now. Hence the slowing trend persists in nominal wages in addition to the outright contraction in work-based incomes in real terms.

While companies, in the aggregate, are no longer shedding labour, there is no evidence that either job openings or new hirings are taking hold. The latest Job Opening and Labor Turnover Survey (JOLTS) data for January showed that U.S. job openings dropped 161k, after a 45k decline in December, and now stand at their lowest level since July 2009 when the economy was barely emerging from the worst recession since the 1930s.

New hires also fell 193k and are now down in six of the past seven months — the lowest they have been since October 2009. The fact that layoffs fell 158k during the month offers little consolation but explains why jobless claims have been trending down at a much faster pace than net employment growth has been picking up. The labour market retains a soft underbelly for an economy soon to be heading into a third year of a post-recession recovery, and it is surprising to see the Fed refrain from reiterating this in the FOMC press statement — though perhaps the central bank is trying to send out an early signal that it is not going to be that quick to usher in QE3 once QE2 runs its course in June.

---today

Thursday, March 17, 2011

Repubs and Demos

Republicans wouldn’t mind a double-dip recession between now and Election Day 2012.

They figure it’s the one sure way to unseat Obama. They know that when the economy is heading downward, voters always fire the boss. Call them knaves.

What about the Democrats? Most know how fragile the economy is but they’re afraid to say it because the White House wants to paint a more positive picture.

---Robert Reich

They figure it’s the one sure way to unseat Obama. They know that when the economy is heading downward, voters always fire the boss. Call them knaves.

What about the Democrats? Most know how fragile the economy is but they’re afraid to say it because the White House wants to paint a more positive picture.

---Robert Reich

Wednesday, March 16, 2011

Monday, March 14, 2011

Friday, March 11, 2011

Why is gold up today?

The 1st March UoM confidence # was 68.2, well below expectations of 76.3 and down from 77.5 in Feb. It’s the lowest since Oct and was likely due to the sharp rise in gasoline prices as one year inflation expectations spiked to 4.6% from 3.4%, the most since Aug ’08 and not far from the level reached in May ’08 of 5.2%. ---Peter Boockvar

Ryan Avent on Government Austerity as a Morality Play (And it's Discontents)

The certain effect of this effort to punish spoiled brats so they learn their lesson is tougher times for workers who didn't necessarily take big mortgages, who didn't necessarily rush into structured financial products, who didn't necessarily want to spend outlandish sums on misguided government initiatives, and who didn't necessarily want to cut taxes on high earners. Their crime is to work in a cyclically vulnerable industry.

If you want to improve the incentives for market participants then improve the incentives for market participants. Support a regulatory system strong enough to allow firms that made bad bets to accept the cost of those bad bets. If Wall Street is spoiled, it's not because interest rates are low. It's because Washington has routinely stepped in to protect big insitutions from failure and has not managed to recover its implicit subsidies after the fact. [source]

If you want to improve the incentives for market participants then improve the incentives for market participants. Support a regulatory system strong enough to allow firms that made bad bets to accept the cost of those bad bets. If Wall Street is spoiled, it's not because interest rates are low. It's because Washington has routinely stepped in to protect big insitutions from failure and has not managed to recover its implicit subsidies after the fact. [source]

Thursday, March 10, 2011

Jobless Claims; China Trade Deficit

Jobless Claims totaled 397k, 21k above expectations and rose from a revised 371k last week. Even with the higher than forecasted reading, initial claims are below 400k for the 4th week in the past 5 and the 4 week average is at 392k. Continuing Claims fell by 20k and Extended Benefits fell by a net 201k. As seen in the recent payroll figures, the labor market is clearly getting better but the process is in fits and starts and the pace of gains still remain mediocre.

China reported an unexpected trade deficit in Feb of $7.3b which was impacted by the Lunar holiday in the beginning part of the month. As trade was pushed into Jan because of the holiday, it’s best to combine Jan and Feb and by doing so, China still reported a deficit of $850mm. Copper is near a 3 month low in response as a moderation in China’s property market is the main priority of central planners. The Yuan also fell to a 2 week low as the trade news may lessen some of the FX political heat on China.

---Peter Boockvar

China reported an unexpected trade deficit in Feb of $7.3b which was impacted by the Lunar holiday in the beginning part of the month. As trade was pushed into Jan because of the holiday, it’s best to combine Jan and Feb and by doing so, China still reported a deficit of $850mm. Copper is near a 3 month low in response as a moderation in China’s property market is the main priority of central planners. The Yuan also fell to a 2 week low as the trade news may lessen some of the FX political heat on China.

---Peter Boockvar

Tuesday, March 8, 2011

One less thing to worry about!

I did not know that Oklahoma had banned Sharia Law!

Thank god. I'm moving there. Now I won't have to worry about being stoned to death.

Thank god. I'm moving there. Now I won't have to worry about being stoned to death.

Rosenbergette:

The Shiller Cyclically-Adjusted P/E now shows an [S&P] overvaluation of close to 40%, a significant jump over the past few months. Sectors that are most overvalued are Financials, Materials, Industrials, while Staples, Tech and Health Care offer the most value.

---Ibid

Bill: Current CAPE10 value = 23.69. Long term average =~ 16.34. Overval = 43%

Some folks say Shiller overstates overvaluation. Eg

---Ibid

Bill: Current CAPE10 value = 23.69. Long term average =~ 16.34. Overval = 43%

Some folks say Shiller overstates overvaluation. Eg

Rosenberg Daily - Oil, Food, Emerging Markets

While there is an estimated $15 per barrel geopolitical risk premium in the oil price, it still pays to take note that before the crisis erupted in the Middle East and North Africa, Brent crude was trading around $100/bbl. This reflects the reality of burgeoning demand from the fast-growing emerging market world (as well as relative energy inefficiencies in this region) coupled with a relatively inelastic supply curve. The same holds true for the food complex, where prices globally have just hit a new record. In the absence of a slowing in demand, the end-result is going to be ongoing increases in headline inflation rates. And if central banks in the emerging market world, who have allowed their economies to overheat as it is, continue to drag their feet in terms of policy tightening, the need for more draconian measures down the road will be even more intense and could well lead to a bad outcome for growth in this part of the world. Inflation in the emerging market world is typically problematic, especially since food comprises such a larger part of the consumer spending basket, but if the supply is inelastic over the intermediate term, then tactics that delay an adjustment to curb demand for other goods and services will likely prove to be the greater of two evils. The tough choices these governments face are generally unappreciated by the investment community. [today]

Vitus Update - Housing Edition

Recently sent to Vitus clients/subscribers

---

Hello

---

Hello

I want to continue in my assigned role as duty curmudgeon, by presenting some recent housing data, most of which I've posted in bits on the blog. But first, some good news:

---

The main reasons housing is hurting include

- Financing. Over 90 percent of recent loan originations have been sold to the GSEs [Government Sponsored Entities: Fannie Mae/Freddie Mac] or securitized with a Ginnie Mae guarantee. There is, practically speaking, no private mortgage lending happening at this time. Banks, big and small, are basically mortgage brokers: They originate and sell. This has been going on, to a greater or lesser extent, for 20 years and more. Here are some discussions about what to do about the mortgage market and the GSE's. If the US can't establish and maintain a private mortgage market, housing as we know it is "inoperative". In any case, any course of action described in the previous link will impact housing prices negatively. For example, one idea is to do away with 30 year loans, and be more like Canada, with 10 year loans. What would that do to housing prices? Exercise left for the reader.

- There is a huge inventory of housing. Six or seven years.

- We have not reached the bottom in house prices. See previous link. Actually, see all these bullett points...

- Also there's forclosuregate

- Appraisals are harder to obtain at asking prices.

- Lenders require Higher down payments and are imposing tighter lending standards

- Unemployment: Long-term and becoming structural. The chart above shows the change in U2: The BLS figure for as-reported unemployment. IMO real unemployment is better shown by U6, which is U2, plus those who are looking for work, those who are working part-time, or those who are temporarily discouraged. U6 is officially at 15.9% as of a week ago. Beyond U6. there are also a lot of permanently discouraged workers - who would work if things obviously improved "enough". These people do not exist officially - they are not counted by the BLS. Many of them are "structurally" unemployed - their skills do not fit into the current workplace. John Williams estimates that this group comprises about 7% of the total potential workforce.

Note of course that economics-wise, housing and employment are analogs, ie, two sides of the same coin. The easy fix to housing is more and better employment, disregarding the hand-wringing above about mortgage finance.

However it's hard to talk about employment without getting into politics. I really don't want to do that here. However, I'll reference a post* I did a while ago to the effect that destroying the middle class is not a winning strategy for leaders, current or aspiring. For some reason, I've received no calls from the White House to further discuss my insights.

---

Market-wise, wow, it's a very confusing time. Basically the market is in wait-mode until June, to see if there will be any more QE's coming from the Fed; the current batch runs out then. A lot of the down-sliding of late in the DOW and S&P is directly attributable to the fact that people are starting to bet that not much more QE will be forthcoming. If you don't see more QE, you can fuggedaboud 40% of the 100% rise in the averages since March of '09. Ie, an S&P of about 1050 is quite possible by year-end.

Gold so far is still doing well. If we do get some kind of new QE in June, Gold is toast for six months+. IMO of course...

Here's David Rosenberg's answer to the investment quandary [ref]:

Start looking for the trend towards consensus growth upgrades we saw take hold last fall to reverse course and along with that a broad investment thrust towards capital preservation strategies, and here are strategies that we like:

- Relative value strategies (true long-short & true hedge funds)

- High quality stocks over low quality stocks

- Dividend yield and growth, including Canadian banks

- Defensive growth over non-resource cyclicals

- Oil and gas equities

- Large cap stocks over small caps stocks

- Low P/E stocks over high P/E stocks

- Corporate bonds

- Precious metals — accumulate on dips

- Ongoing overweight to Canada and the Canadian dollar

- Hybrid funds that carry a yield better than one can get in the government bond market and with low beta to the overall stock market.

Comments: The following are not recommendations; they are examples.

- For many of us, true long-short investment through hedge funds is not an option so much. However there are a lot of mutual funds and even etf's which do this. SWHEX. CSM.

- High quality means long-term profitability and dividend paying, good financials, and industry prominence. Examples are KO, PG, MCD, WMT, and even MSFT.

- The dividend and low P/E themes overlap High Quality. There are a lot of dividend ETF's such as DTN, SDY, DVY, and VIG to name a few.

- Oil and gas: COP, XON, OIH, XES

- Precious metals: PHYS, SGOL

- Canada: EWA. Whoops. EWC. EWA ain't bad...

- Hybrid funds: PTTDX

I could type more ticker symbols.

Rosie has been consistently positive on treasuries and muni bonds, although he's been burned on that recently so I think the bond theme is embedded in the hybrid theme he mentions. But he did mention muni's as late as today. Most of punditland swears up and down that treasuries and munis are toast. I'm with Dave - the equity boom will un-boom, but not if the Fed announces or hints at more Quantitative Easing.

I hope the above is interesting, or useful, or at least amusing.

Bill

* Beware of this link: Material inconsistant with "conservative" views.

Update

Rosenberg today says: There is a great debate both in the markets and among Fed officials about whether QE3 will be necessary. Atlanta’s Lockhart was the latest to voice his view that such will be unwarranted, and he seems to find support from the likes of Richard Fisher from Dallas and Charles Plosser from Philadelphia. But there are others like Janet Yellen and Bill Dudley who appear to desire even more doses of stimulus. Bernanke is keeping his cards close to his vest. All we can say is that by the time the decision will be made, the headline U.S. inflation rate is very likely going to be at or above 3%, so the Fed is going to have a real job on its hands to convince everyone that “core” is the measure to watch (though even here we can expect to see fuel kick into airlines and cotton seep into apparel).

Not only that, but with European Central Bank’s (ECB) Trichet saying that a euroland rate hike is “possible” next month to combat rising inflation and mentioning those two sabre-rattling words “strong vigilance” after last week’s policy meeting, it would seem that if the Fed were to ease monetary policy at a time when the ECB is snugging liquidity would seem to be a prescription for a disastrous result for the U.S. dollar.

Bill: So - this wrinkle says: If Fed and ECB diverge, gold UP, not down. sigh.

Update

Rosenberg today says: There is a great debate both in the markets and among Fed officials about whether QE3 will be necessary. Atlanta’s Lockhart was the latest to voice his view that such will be unwarranted, and he seems to find support from the likes of Richard Fisher from Dallas and Charles Plosser from Philadelphia. But there are others like Janet Yellen and Bill Dudley who appear to desire even more doses of stimulus. Bernanke is keeping his cards close to his vest. All we can say is that by the time the decision will be made, the headline U.S. inflation rate is very likely going to be at or above 3%, so the Fed is going to have a real job on its hands to convince everyone that “core” is the measure to watch (though even here we can expect to see fuel kick into airlines and cotton seep into apparel).

Not only that, but with European Central Bank’s (ECB) Trichet saying that a euroland rate hike is “possible” next month to combat rising inflation and mentioning those two sabre-rattling words “strong vigilance” after last week’s policy meeting, it would seem that if the Fed were to ease monetary policy at a time when the ECB is snugging liquidity would seem to be a prescription for a disastrous result for the U.S. dollar.

Bill: So - this wrinkle says: If Fed and ECB diverge, gold UP, not down. sigh.

Monday, March 7, 2011

Labor market getting better?

DeLong shows a chart from the Council of Economic Advisors, Austan Goolsbee, chair.

Bill: This is MOM change. I don't trust it - I think you have to deal with what goes on in U6 unemployment in any employment pronunciation. But, it can be argued that there is some good news I guess.

Bill: This is MOM change. I don't trust it - I think you have to deal with what goes on in U6 unemployment in any employment pronunciation. But, it can be argued that there is some good news I guess.

Krugman - Republicans, generally, sneak in under the fence; Democrats buy tickets

...until 1980 or so the United States generally paid its way; the ratio of debt to GDP generally fell over time. Then starve-the-beast came to power, and fiscal realism went away. That’s the story; anyone who glosses over that, who makes it a plague-on-both-houses issue...is in an essential way misleading his readers.

Bear in mind, too, that the signature initiatives of Republican presidents — the Reagan tax cut, the Bush tax cut, the Medicare drug benefit — have all been unfunded deficit-raisers; the signature initiatives of Democratic presidents — the Clinton tax hike, Obamacare — have all been deficit-reducing. (Yes, ...Bush I’s tax increase was an exception, but the GOP has made it clear that nothing like that will ever happen again.)

Democrats aren’t fiscal saints. But we have one party that has been generally responsible, and tries to pay for what it wants, and another party that consistently, deliberately, takes actions to increase deficits in the long term. Saying this may be shrill; but not saying it is being deceptive.

---source

Bear in mind, too, that the signature initiatives of Republican presidents — the Reagan tax cut, the Bush tax cut, the Medicare drug benefit — have all been unfunded deficit-raisers; the signature initiatives of Democratic presidents — the Clinton tax hike, Obamacare — have all been deficit-reducing. (Yes, ...Bush I’s tax increase was an exception, but the GOP has made it clear that nothing like that will ever happen again.)

Democrats aren’t fiscal saints. But we have one party that has been generally responsible, and tries to pay for what it wants, and another party that consistently, deliberately, takes actions to increase deficits in the long term. Saying this may be shrill; but not saying it is being deceptive.

---source

Friday, March 4, 2011

Rosenberg Daily - What Happens after QE2?

The answer(s) is hardly complicated since we have a template for this in 2010. It is a very simple guidepost.

Last year, from April 23rd through to August 27th, the Fed allowed its balance sheet to shrink from $1.207 trillion to $1.057 trillion for a 12% contraction as QE1 drew to a close. Go back a year to the Federal Open Market Committee minutes and you will see a Federal Reserve consumed with forecasts of sustainable growth and exit strategy plans. A sizeable equity correction coupled with double-dip fears were nowhere to be found.

Now over that interval ...

So who buys the bonds when Ben leaves the building?

The same folks who were the buyers last year from April to August. The ones who were switching out of equities, commodities, and other risk-assets.

Now you know how to play the second half of the year!

---Yesterday

Last year, from April 23rd through to August 27th, the Fed allowed its balance sheet to shrink from $1.207 trillion to $1.057 trillion for a 12% contraction as QE1 drew to a close. Go back a year to the Federal Open Market Committee minutes and you will see a Federal Reserve consumed with forecasts of sustainable growth and exit strategy plans. A sizeable equity correction coupled with double-dip fears were nowhere to be found.

Now over that interval ...

- S&P 500 sagged from 1,217 to 1,064.

- S&P 600 small caps fell from 394 to 330.

- The best performing equity sectors were telecom services, utilities, consumer staples, and health care. In other words — the defensives. The worst performers were financials, tech, energy, and consumer discretionary.

- Baa spreads widened +56bps from 237bps to 296bps • CRB futures dropped from 279 to 267. • Oil went from $84.30 a barrel to $75.20. • The VIX index jumped from 16.6 to 24.5.

- The trade-weighted dollar index (major currencies) firmed to 76.5 from 75.5.

- Gold was the commodity that bucked the trend as it acted as a refuge at a time of intensifying economic and financial uncertainty — to $1,235 an ounce from $1,140 and even with a more stable-to-strong U.S. dollar too.

- The yield on the 10-year U.S. Treasury note plunged to 2.66% from 3.84%.

So who buys the bonds when Ben leaves the building?

The same folks who were the buyers last year from April to August. The ones who were switching out of equities, commodities, and other risk-assets.

Now you know how to play the second half of the year!

---Yesterday

Today's Job Numbers

Peter Boockvar:

Barry Ritholtz:

In January alone, a whopping 319,000 people dropped out of the workforce. In February (this months' report) another 87,000 people dropped out of the labor force.

Were it not for people dropping out of the labor force, the unemployment rate would be over 11%...

Looking ahead I strongly doubt the reports will be this good over the course of a year.

- February Payrolls rose by 192k, 4k less than expected but private sector job gains totaled 222k, 22k above forecasts

- Payrolls averaged 128k over the two months and 145k in the private sector. It’s certainly an improvement but still lackluster at this stage of an economic rebound

- The unemployment rate ticked down by .1% to 8.9% encouragingly led by a 250k increase in the household survey

- The labor force rose by 60k after the sharp decline over the past 2 months

- The all-in U6 rate fell .2% to 15.9%.

- Average hourly earnings was flat vs an expected .2% gain and is up just 1.7% y/o/y

- Manufacturing added jobs for a 4th month.

Barry Ritholtz:

- Private job growth accelerated and the unemployment rate fell for the third straight month; Since the February 2010 low, total payroll employment has grown by 1.3 million.

- Average hourly earnings of all employees increased by one cent to $22.87, up 1.7% year over year.

- The average work week for all workers was flat at 34.2 hours.

- Among all industries, 68.2% were hiring, up from 60.1% in January. This is the broadest range of hiring since May 1988.

- Revisions were all positive: Payroll rose in December and January by a cumulative 58,000. A revised 152,000 in December and by 63,000 in January.

- Unemployment dropped by 190,000 to 13.7 million; Employment gained 250,000 to 139.6 million.

- The Labor participation rate was unchanged at 64.2%; the employment-population ratio at 58.4% was also unchanged in February

- Sectors that added jobs include Manufacturing (+33,000), Construction (+33,000), Professional and business services (+47,000), Health care (+34,000), Transportation and warehousing (+22,000),

- Sectors losing jobs were State and Local government

Mish:

This was a solid jobs report, not as measured by the typical recovery, but one of the better reports we have seen for years. Moreover, 30,000 government jobs bit the dust. The higher that number, the better off we will all be. +212,000 private jobs is a good number. However, I suspect this may be as good as it gets for a while.

At the current pace, the unemployment number would ordinarily drop, but not fast. However, many of those millions who dropped out of the workforce could start looking if they think jobs may be out there. Should that happen, the unemployment rate could rise, even if the economy adds jobs at this pace...

In the last year, the civilian population rose by 1,853,000. Yet the labor force dropped by 312,000. Those not in the labor force rose by 2,165,000.

At the current pace, the unemployment number would ordinarily drop, but not fast. However, many of those millions who dropped out of the workforce could start looking if they think jobs may be out there. Should that happen, the unemployment rate could rise, even if the economy adds jobs at this pace...

In the last year, the civilian population rose by 1,853,000. Yet the labor force dropped by 312,000. Those not in the labor force rose by 2,165,000.

In January alone, a whopping 319,000 people dropped out of the workforce. In February (this months' report) another 87,000 people dropped out of the labor force.

Were it not for people dropping out of the labor force, the unemployment rate would be over 11%...

Looking ahead I strongly doubt the reports will be this good over the course of a year.

Thursday, March 3, 2011

Bank "profits". Not.

Many of the bailouts, mortgage mods and behaviors we have today exist to serve a single purpose: To allow the banks to kick the can down the road as far as they possibly can when it comes top their dual portfolio of bad mortgages and bank owned Real Estate (REOs)...

Rather than go Swedish, and force a shorter painful pre-packaged bankruptcy process, we have opted to take the long slow route:

Once a home goes into foreclosure, the accounting changes: It is now a loss that must be written down immediately. That hits the banks capital levels. Consider what the next 3-5 million foreclosures will do to banks’s capital cushions.

Once a foreclosure occurs, not only does the capital write down take place, but the local property tax liability accrues to the bank; prior to foreclosure, the liability is to the nominal home owner and/or property. Once the bank takes possession, its on them.

Hence, you can see why “Extend & Pretend” is so attractive to the large institutions sitting on massive REO inventory, enormous bad loans and CDOs, and huge future local tax obligations.

---Barry Ritholtz

Rather than go Swedish, and force a shorter painful pre-packaged bankruptcy process, we have opted to take the long slow route:

1) Banks are slowly rebuilding their capital by borrowing from one branch of government and lending to another. This is a slow process, but its less well unerstood (and hence more politically acceptable) than merely giving Banks capital outright.Under normal circumstances, the bad mortgage process goes Delinquency (late payments) Default (90 days behind), Foreclosure (legal proceedings to enforce the note).

2) FASB 157 allows banks to carry all of these structured products made of bad mortgages on their books indefinitely.

3) Banks are carrying lots of housing inventory waiting for a better residential market to emerge 5 or 10 years down the road.

Once a home goes into foreclosure, the accounting changes: It is now a loss that must be written down immediately. That hits the banks capital levels. Consider what the next 3-5 million foreclosures will do to banks’s capital cushions.

Once a foreclosure occurs, not only does the capital write down take place, but the local property tax liability accrues to the bank; prior to foreclosure, the liability is to the nominal home owner and/or property. Once the bank takes possession, its on them.

Hence, you can see why “Extend & Pretend” is so attractive to the large institutions sitting on massive REO inventory, enormous bad loans and CDOs, and huge future local tax obligations.

---Barry Ritholtz

Subscribe to:

Comments (Atom)